Part I: Analysis of Correlations Between Private Security Presence and Insurance Claims & Security-Related Lawsuits

Key points

- Private security now often outnumbers police, making private–public policing arrangements a central feature of contemporary public protection.

- Higher density and professional training of guards correlate with fewer insurance claims, lower premiums, and reduced premises-liability lawsuits.

- Evidence-based investment in security personnel and integrated security systems typically returns $3–$6 for every $1 spent through avoided losses, legal costs, and improved underwriting.

The very nature of “public safety” has been in transition; due, in part, because in many countries private security has seen significant growth while there has been stagnation — and even force reductions — in public police.

This re-balancing in public protection makes it important for governments, insurers, and academics alike to better understand the contributions of private security officers.

A U.S. National Institutes of Justice report plainly outlines the imperative: with private security personnel often outnumbering police officers, it has become impossible to ignore the extent and pervasiveness of private policing arrangements. Being “for” or “against” private security is both no longer relevant nor helpful, according to the study (“Managing the Boundary Between Public and Private Policing,” New Perspectives in Policing, NIJ/John F. Kennedy School of Government at Harvard University).

The relevant question at hand is: What does it mean for public safety? Primarily examining data from Europe and the U.S. over the last three years, the International Security Ligue conducted public data research analyzing sectoral studies, insurance claims, legal verdicts, academic research, and industry trends.

The goal? To answer a policy-relevant question: Does a higher per capita presence of private security officers correlate with tangible benefits in public safety, risk mitigation, and legal or insurance outcomes?

Intersection of Insurance & Security Personnel

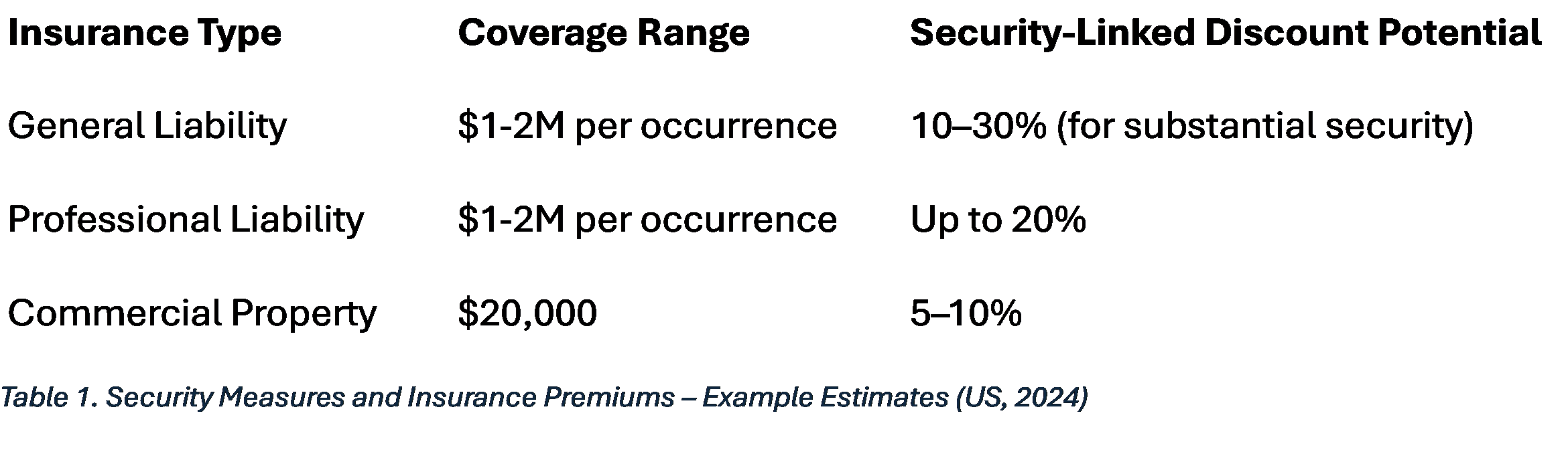

Private security's impact on insurance claims is multi-faceted. In several lines of commercial property and casualty (P&C) insurance—especially those covering liability, theft, fraud, and premises risks—underwriters explicitly include the presence and density of trained security personnel as criteria, alongside use of surveillance technology and a history of prior incidents. Repeated claims, a history of lawsuits, or the absence of onsite security can sharply raise a company’s annual rates.

U.S. Findings. An AI meta-analysis of US insurance underwriting practices shows a preference for properties and businesses that demonstrate active risk mitigation through visible physical security measures, including guard density, training records, and integrated response protocols.

Empirical industry reports show that higher per capita security presence demonstrably lowers insurance claims and property damage costs for clients in sectors like retail, hospitality, and commercial real estate. As loss prevention outcomes improve, insurers pass risk savings on to businesses in the form of lower premiums or improved terms. Conversely, when claims rise (e.g., theft or premises liability), insurers typically respond by demanding improved security or raising premiums. Together, these forces create a strong financial incentive for security investment.

- Retail: 2024 data from the National Retail Federation show that US retail theft (shrink) exceeded $112 billion in 2024, with over a third due to shoplifting and another third to employee theft. Case studies reveal that adding or increasing trained guard presence at retail chains directly reduces incident rates, shrinkage, and results in lower insurance payouts (The Impact of Retail Theft & Violence 2024, NRF)

- Property/Liability: Guarded commercial properties see insurance claims reduce by up to 30% in peer-matched studies, and this operational improvement is often reflected in premium reductions following audits confirming heightened security practices (New Realities and New Solutions in Public and Private Policing, Handbook on Public and Private Security, Nov. 2023).

- Business Improvement Districts (BIDs): Programs in Los Angeles, Chicago, and Atlanta that combine private security presence with integrated surveillance networks have reported decreases in property-related insurance claims, attributed to both deterrence and faster incident response times.

Adding or increasing trained guard presence at retail chains directly reduces incident rates, shrinkage, and results in lower insurance payouts — National Retail Federation

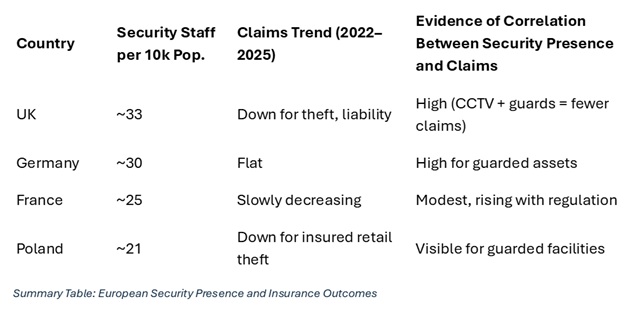

European Findings. Compared to the U.S., Europe has lower levels of both insurance penetration and private security employment per capita, but the gap has been closing. Rapid urbanization, higher incidences of organized retail crime, and regulatory nudges (such as the UK’s PROTECT Duty) are driving more investment in private security, with correlating effects on insurance markets.

Across Europe, insurers are advocating not just for security officers, but for integrated “security ecosystems” (security personnel plus surveillance plus access control), which are now part of standard risk evaluations. Germany, France, Poland, and the UK represent significant markets, collectively employing several hundred thousand licensed private security professionals, often as a legal or contractual requirement for insurers.

What's the impact? Data from the European Insurance and Occupational Pensions Authority (EIOPA) show that European countries with higher private security density overall (e.g., UK, Germany) report fewer high-value claims per insured asset—particularly when improved security protocols are empirically verified by insurers during audits.

In Germany, for example, industry analysis show that insurers increasingly tie premium terms and policy renewals to verified risk mitigation measures. Commercial clients with effective physical security programs featuring robust security personnel staffing typically receive improved underwriting outcomes, including lower claims frequency and more favorable renewal terms (Allianz Global Insurance Report 2025: Rising demand for protection, May 2025; Pulse Check – State of the European Insurance Industry, Information Services Group. Inc., 2024; and Insurance industry in Germany - Statistics & Facts, Statista, Jan. 2025).

European countries with higher private security density report fewer high-value claims per insured asset.

And there is similar evidence that U.K., French, and Polish insurers increasingly require evidence of effective physical security (i.e., staff on premises, ongoing staff training) as preconditions for liability coverage at favorable rates.

Security-Related Lawsuits and Security Presence

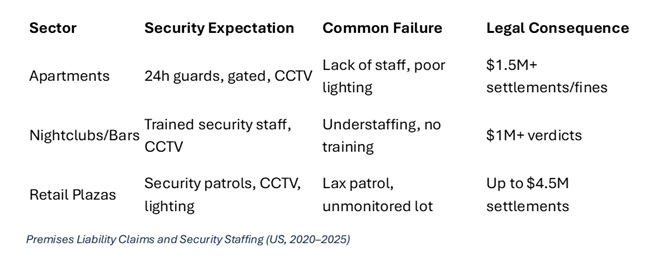

Civil litigation against property owners for "negligent security" is one of the fastest-growing segments of premises liability law in the U.S. Jury verdicts and settlements in these cases have risen sharply over the past decade; average settlements and median jury awards exceed one million dollars per incident for most industries.

Such lawsuits are far less common in Europe, but while there is no single European dataset that tracks all negligent physical premises security lawsuits, anecdotal evidence suggests—if there is a trend—that is probably indicates growing risk for premises owners who fail to provide security commensurate with foreseeable threats.

Do more officers reduce risk? In the U.S., negligent security cases and premises liability lawsuits increasingly cite the absence, insufficiency, or poor training of guards as proximate causes for failing to prevent injury, loss, or death. Several major verdicts have explicitly linked insufficient security staffing to liability.

Especially in known “hot spots,” which make criminal acts “foreseeable,” courts have repeatedly ruled that under-staffing, cost-cutting (hiring one guard when four were deemed needed), and skipped patrols represent a breach of duty for property or business owners.

In Europe, the presence and training of security officers are increasingly referenced as evidence of compliance with duty of care; increasing the likelihood that their absence could be deemed a breach, which can expose a business to administrative penalties, having their insurance dropped, or costly civil judgments.

College of Policing Crime Reduction Toolkit data indicate that layered security (CCTV plus officers plus lighting) yields up to a 34% reduction in targeted crime, with claims and settlements showing similar downward trends in venues meeting these standards.

Sectoral analysis shows businesses that employ and retain professional guards with ongoing training face fewer and less severe claims—a trend noted in insurance underwriter guidance.

Especially in high-risk sectors, data suggest that the density and professionalism of private security officers correlate with measurable reductions in liability incidents, insurance claims, and associated legal costs in U.S.

But is it worth the cost?

The evidence is pretty plain: deploying more security officers reduces risk and liability and improves insurance terms. But are benefits worth the expense? More research is needed for exact calculations, but a meta-review of available information indicate the answer is a resounding "yes."

- Industry studies and insurance models consistently show that the cost of higher private security staffing is significantly lower than the cumulative costs associated with uninsured or poorly mitigated claims, lawsuits, and lost assets.

- Real-world cost-benefit analyses (CBAs) document that spending $1 in proactive security investment can prevent $3–$6 in losses, legal costs, and insurance premium hikes.*

- The ROI of physical security is also realized through lowered deductibles, higher policy renewal rates, and greater investor confidence, serving as a form of operational “insurance within insurance.”

In short, cost-benefit calculation consistently favors proactive investment in security presence, as the legal, financial, and reputational costs of negligence or under-investment are now demonstrably higher than the ongoing expense of professional risk mitigation.

Part II will examine correlations between the density and quality of a private security presence and embezzlement, theft, and other quantifiable risk indicators.

*This cost-benefit estimate is derived from industry case studies and insurance modeling referenced in sectoral analyses of retail, commercial property, and liability risk. While there is no single, universal source for the "$1 saves $3–$6" ratio, similar returns on investment have been documented in adjacent domains such as workplace safety (U.S. Department of Energy, ASSE), disaster mitigation (National Institute of Building Sciences), and risk management. The Ligue’s estimate reflects a synthesis of empirical findings from insurance underwriting practices, legal verdicts, and operational audits across the U.S. and Europe.