Key Points

- Cash deserts are expanding worldwide, driven by long term declines in bank branches and ATMs across advanced and emerging economies.

- The consequences are severe — from exclusion of vulnerable populations to weakened resilience during outages, crises, and system failures.

- Regulation should ensure effective access to cash through the obligation for credit institutions to maintain a minimum distribution network for ATMs and bank branches.

Moving away from physical currencies toward digital payments is heavily marketed as being frictionless and super-efficient, but it has a troubling by-product that requires attention: cash deserts. These are communities where access to cash — in the form of bank branches, ATMs, or cash services — has eroded to the point of exclusion. Far from being a benign by product of digitalization, cash deserts are creating new inefficiencies, deepening inequality, and exposing societies to systemic risk.

Desertification

Across advanced and emerging economies, access to cash infrastructure has been shrinking. Bank branch closures have accelerated, ATM networks have contracted, and rural and low income communities have been disproportionately affected.

In Europe, the European Central Bank routinely reports on a declining number of bank branches and ATMs. Most recently, ECB reported that the ATM count was 2.9% lower at the end of the first half of 2025 than at the end of the first half of 2024 (Payment statistics: first half of 2025, ECB Press Release, January 29, 2026) and an even greater reduction in the number of bank offices. “The structural financial indicators show a further decline in the number of bank offices in the EU, averaging 3.41% across Member States. Decreases were observed in 25 of the 27 countries, ranging from -0.71% to -12.48%.” (EU structural financial indicators: end of 2024, ECB Press Release, June 2025).

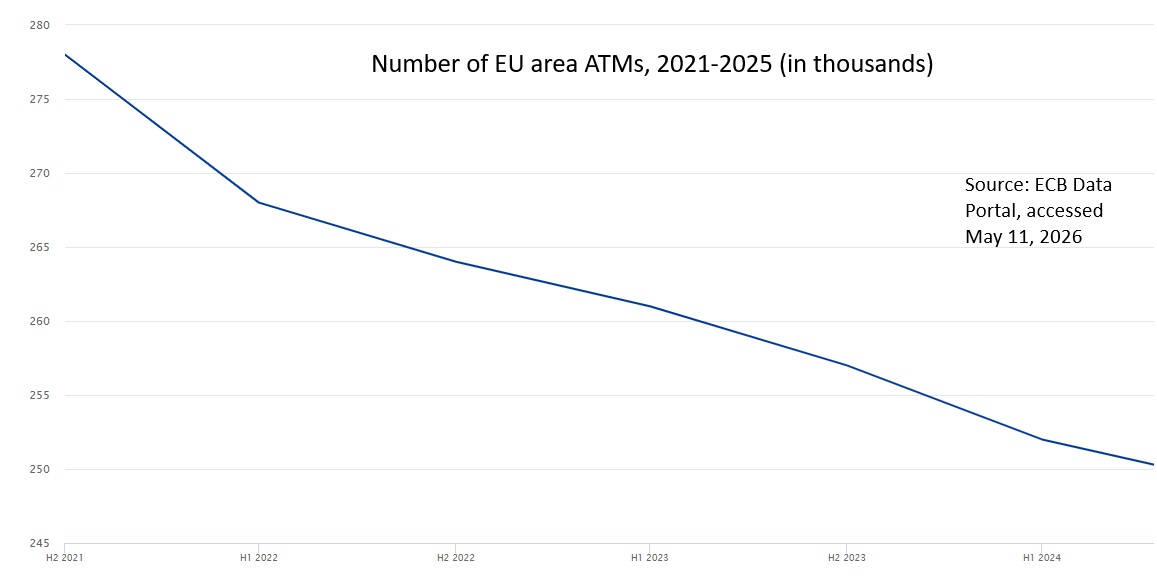

Queries of the ECB Data Portal reveal that the latest figures are part of a long-term trend. Since 2021, there has been a substantial and steady decline in the total number of ATMs across the euro area (see figure), and estimates are that the number of bank branches fell by 36% between 2008 and 2022.

The United Kingdom has seen similar patterns. Around 6,700 bank and building society branches have closed and the number of ATMs has fallen by 40% since 2015, according to data cited by the UK Parliament’s House of Commons library (Access to cash and banking services, Research Briefing, March 16, 2026).

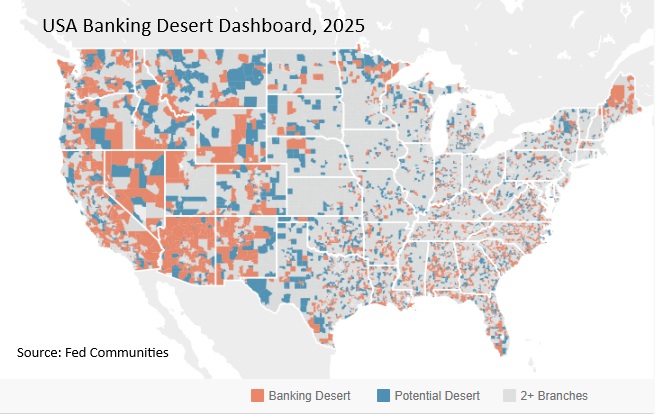

In the United States, Fed Communities, a collaboration among the 12 Reserve Banks of the US Federal Reserve System, compiles data on the distance people must travel to get to a bank, concluding that, in 2025, 4% of statistical neighborhoods are banking deserts, with another 4% one branch closure away from becoming one. While cash remains essential for millions, branch closures have accelerated in rural and low-income counties, creating widening gaps in access. (Banking Desert Dashboard, Fed Communities, Nov. 3, 2025.)

Emerging economies are not immune. In Kenya, the Central Bank has frequently documented and discussed the decline in physical bank branches and ATMs. In 2023 in Nigeria, a humanitarian issue resulted from a massive cash shortage during a botched attempt to redesign the naira, exposing how fragile access can be when cash distribution networks are thin.

Consequences

Cash deserts are not merely an inconvenience — they are a structural threat to financial inclusion, economic resilience, and social cohesion.

Older adults, people with disabilities, migrants, and those with limited digital literacy rely disproportionately on cash, likely one of the drivers for why more than 60% of the euro area population considers having the option to pay with cash to be essential (ECB Study on the Payment Attitudes of Consumers in the Euro Area).

A dwindling cash infrastructure also creates economic inefficiencies. When cash access disappears, people must travel farther to withdraw money — imposing time and transport costs. Small businesses in cash dependent communities face reduced sales and higher risks.

And then there are resilience risks. Cash is the only payment instrument that functions during power outages, cyber incidents, or network failures. Economic leaders have repeatedly emphasized cash’s role as a “public good” and a critical backup in crises.

Finally, desertification creates an erosion of trust. When citizens cannot access their own money, confidence in financial institutions and public authorities erodes — a dynamic observed in past cash crises.

Pushing Back

There exists rising public pressure to end cash deserts. In Junee, New South Wales, some rural communities mounted sustained resistance to the disappearance of in-person banking, protesting Commonwealth Bank’s announcement to close their last remaining branch. The public backlash — citing poor digital connectivity and the exclusion of elderly and digitally limited customers — helped trigger a Senate inquiry into regional bank closures, and in 2025 the federal government secured a national agreement from the Big Four banks — Commonwealth Bank, ANZ, NAB, and Westpac — to halt all regional branch closures until July 2027. (“Regional bank closure moratorium,” About Regional, Feb. 16, 2025.)

An expanding and diverse coalition of organizations have become increasingly vocal about the problems created by a dwindling cash infrastructure, from the National Community Reinvestment Coalition in the U.S., which fights for economic justice to Quarriers in Scotland, a large social care charity that has raised awareness about how the lack of free ATMs impacts people with disabilities.

An expanding and diverse coalition of organizations have become increasingly vocal about the problems created by a dwindling cash infrastructure.

More lawmakers are also starting to take notice of the problem, like Martin Rhodes, a Scottish Labour Party politician who has been Member of Parliament for Glasgow North since July 2024. “The shift to card-only businesses and the closure of free-to-use ATMs are leaving people unable to spend their own money,” he said during a House of Commons debate in October 2025. “In my constituency, we have seen a 22% decrease in free-to-use ATMs between 2019 and 2025. This has created cash deserts, where communities are left without access to cash machines, and those that remain [are] often charged for withdrawals or are inside premises with closing times.”

Calls for Change

Cash can only function as legal tender if it is both accepted in practice and reliably accessible. International organizations, consumer groups, and policymakers are increasingly calling for action to address the problem of cash deserts, including the European Consumer Organisation, an umbrella group for 42 independent consumer groups from 31 countries.

Ultimately, credit institutions should bear primary responsibility for ensuring access to cash, while the wider cash ecosystem should be recognized as supporting actors and not be subject to disproportionate regulatory obligations. Regulation should, for example, ensure effective access to cash through the obligation for credit institutions to maintain a minimum distribution network for ATMs and bank branches, guaranteeing that the basic cash withdrawal services remain available and free of charge for their customers.

Some countries have made more progress than others in ensuring cash access. In 2023, for example, the Netherlands passed legislation requiring banks to maintain minimum cash access standards and mandating DNB oversight of ATM reductions. The Cash Payments Act is expected to be finalized in 2026, and mandates banks maintain a minimum nationwide ATM infrastructure (5 km max distance) and tasks DNB with overseeing cash availability. (“Many cash laws and regulations forthcoming,” Feb. 10, 2025.)

Others seem to be getting on board. Sweden, for example, had faced intense public criticism for allowing for allowing rapid ATM and branch reductions without adequate safeguards, but new proposals aim to mandate that banks provide cash services and businesses accept cash to ensure (“Sweden Reverses Course: Cash Returns as a Matter of Survival, Inclusion and Security,” Cash Essentials, May 21, 2025.)

A Model Vision

Austria stands out as a country where the central bank has taken proactive responsibility for safeguarding cash access.

The Oesterreichische Nationalbank (OeNB) has explicitly framed cash as a strategic asset requiring active stewardship. As Matthias Schroth, Director of Legal, Cash Management & Equity Interests at OeNB, states: “The OeNB has deliberately opted for a strategy of active neutrality and the cultivation of its premium product cash. We are not waiting, we are shaping the market together and we are actively securing freedom of choice, among other things through our initiative to install cash dispensers in structurally weak regions. The result: Austria remains one of the countries with a strong cash preference among the population. Our mission remains clear. A modern payment system needs diversity, freedom of choice and robustness. Cash is indispensable for this. Cash is modern, secure and humane.”

Austria’s approach — including OeNB supported ATM installations in underserved regions — demonstrates what central bank leadership looks like in practice.

The OeNB has deliberately opted for a strategy of active neutrality and the cultivation of its premium product cash. We are not waiting, we are shaping the market together and we are actively securing freedom of choice, among other things through our initiative to install cash dispensers in structurally weak regions.

Central Banks as “Product Managers” for Cash

Ending cash deserts is supported by a shift in mindset, where central banks do not merely issue banknotes but accept responsibility the functioning of the cash ecosystem. Cash is, in effect, a product — one that requires maintenance, distribution, promotion, and resilience planning. A product without support degrades and without distribution risks disappearing.

A “product manager” mindset would help to encourage:

- ensuring universal access,

- monitoring infrastructure health,

- intervening when markets fail, and

- championing cash as a pillar of payment resilience.

Key Takeaway. Cash deserts are not an inevitable by-product of modernization — they are a policy failure with real consequences: exclusion of vulnerable citizens, weakened resilience, rising costs from fragmented fee structures, and the erosion of freedom of choice. Cash is a product that needs support like any other, requiring active stewardship, and countries taking leadership are demonstrating what is possible.